One Of My All-Time Early Buffett Investments Favorites

A Workout: British Columbia Power.

An Almost Risk-Free Bet

One day, my girlfriend asked me: ‘‘Isn’t there always some risk when you invest?’’

I told her: ‘‘Not necessarily. Occasionally, there are rare and obscure situations where you can earn attractive returns while taking almost no risk at all.’’

She smiled and pushed back: “You said ‘almost’ - so there must still be risk.”

I replied: ‘‘The investment itself can be risk-free. What remains is counterparty risk - the chance that one party in a transaction fails to perform. And that risk, my love, is about the same as the risk of not getting your deposit back if your bank defaults.”

In other words, the structure can be safe even when life is not.

I care far more about protecting my principal than chasing growth for its own sake. And when people think of Warren Buffett’s greatest investments, their minds usually jump to Coca-Cola, Apple, or American Express. Rarely does British Columbia Power make the list of his early deep value investments.

It should.

The investment did not deliver a multi-bagger. But it did deliver something far more important: a very high return relative to no risk taken and thus a VERY high risk-adjusted IRR achievable.

British Columbia Power is a reminder that Mr. Market occasionally offers near risk-free opportunities in obscure deep value stocks. The discipline lies in recognizing them - and the conviction lies in sizing up when they appear, just as Charlie Munger did.

I wrote this note about being a “know-something” investor, and British Columbia Power is a perfect case study in that mindset: betting heavily on asymmetrical outcomes. Or, in Buffett’s words, a classic workout - a special situation investment firmly within his circle of competence.

Investing in Outcomes, Not Stories

In Buffett’s early partnership letters, investments were grouped into three buckets:

Generals

Controls,

Workouts.

A workout is a special situation investment where the return does not depend on business performance or market optimism, but on a specific corporate event being resolved. These events could include liquidations, mergers, restructurings, or legal settlements among others. The key feature of a workout relates to the value which in turn is unlocked by time and process, not by growth or multiple expansion.

In Buffett’s words, the outcome was largely independent of whether the stock market went up or down. What mattered was whether the event played out as expected. Workouts therefore offered a different type of risk: not economic risk, but event risk - a classic setup for deep value and risk arbitrage investors. And when the odds were favorable, they allowed capital to compound without needing a bullish market.

The Corporate Event: A Utility Being Taken Over

This workout originated from a dispute between British Columbia Power and the newly formed British Columbian government of William Andrew Bennett. It all started when the province took steps in relation to expropriating British Columbia Power’s primary asset and subsidiary - British Columbia Electric.

British Columbia Electric was a regulated electric and gas utility company providing electricity to residents of B.C. and the largest electricity generator at that time. The Bennett government had a vision for hydro power generation, however. They wanted to expand the hydro power-generation and therefore sougt to construct dams along the Peace River.

Bennett’s idea was to harness both the Peace River and the Columbia River at the same time in order to secure long-term hydroelectric supply for the province. The plan, later referred to as the “Two Rivers Policy,” would generate more electricity than domestic demand required, making it possible to export surplus power to the United States.

A little historic gem on Bennett’s visions for B.C.’s hydroelectricity future can be found in this clip from 1961 (thanks for the vivid internet).

The dominant electricity and gas provider in the province, British Columbia Electric was the natural counterparty for purchasing the output from the Peace River project. A separate private entity, the Peace River Power Development Company, needed a long-term supply agreement with the utility in order to raise the capital required to construct the dams. British Columbia Electric refused to commit, which effectively stalled the project.

After months of growing frustration and increasing political pressure, Bennett decided to act. In August 1961, following persistent takeover rumors, he introduced the Power Development Act in the provincial legislature. The law authorized the government to expropriate British Columbia Electric for C$111 million. It also included an offer to acquire the remaining shares of British Columbia Power (the holding company) for C$68.6 million, with interest accruing until the offer expired in July 1963. In total, the transaction implied a combined value of approximately C$179.6 million.

The Revised Offer And The Duo Steps In

Eight months after the initial takeover, the British Columbian legislature enacted two new laws. One of them amended the Power Development Act by increasing the compensation paid to British Columbia Power for British Columbia Electric by an additional C$60.8 million. At the same time, the amendment withdrew the government’s earlier offer to purchase the remaining assets of the parent company.

At this point in time, British Columbia Power had net cash deducted all liabilities of around C$19 per share. The stock traded at a price around C$16-17 a share. That is a dollar at 80 to 90 cents.

Further, British Columbia Power held around C$2 a share in additional assets and had a free call option on possible continued upside from the ongoing litigation related to additional compensation. It was at this point that Munger, with his newly formed partnership, and Buffett made their move.

Munger put in not just his whole partnership, but all the money he had, and all that he could borrow into the arbitrage on this single investment. Maybe Munger felt even more within his circle of competence, as he used to be a lawyer and understood the legal mechanics behind this special situation investment and hence sized the position up compared to Buffett.

The Debentures Issued By Electric

There was still one technical loose end that Buffett and Munger had to get comfortable with before leaning into the position.

British Columbia Electric, the main operating asset of British Columbia Power, had previously issued debentures that were convertible into shares of the parent company. Bondholders had the right, at their own choice, to exchange their debt for common stock in British Columbia Power. This setup made sense as long as British Columbia Power fully owned British Columbia Electric. Once the subsidiary was expropriated, however, the logic collapsed. A conversion would now wipe out debt tied to an entity the parent no longer controlled, while forcing British Columbia Power to issue new equity in return.

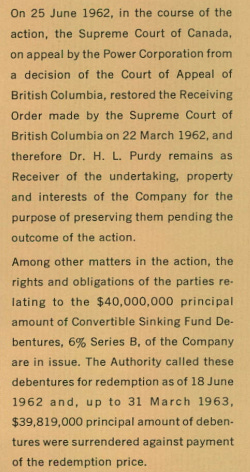

The courts therefore had to decide two things: whether these debentures still carried valid conversion rights into British Columbia Power shares, and whether any newly converted shareholders would be entitled to a large cash distribution that had already been paid out in December 1961. To guard against an unfavorable outcome, the Supreme Court of British Columbia required British Columbia Power to retain C$20 million in cash in case debenture holders were ruled eligible and chose to convert en masse.

In practice, this risk was far smaller than it appeared. First, the provincial government explicitly assumed responsibility for the debenture debt as part of the expropriation, making it clear that the liability no longer sat with British Columbia Power. Second, the issue largely resolved itself after the passage of the Amending Act, when the British Columbia Hydro and Power Authority called the debentures in May 1962.

By the end of June, roughly C$39.8 million of the original C$40 million issue had already been redeemed. Only about C$0.2 million remained outstanding by the time the court eventually ruled in 1963.

Even if the court had tried to unwind the redemptions, doing so would have been administratively chaotic. Despite how threatening the situation looked on paper, it was effectively a non-event for common shareholders.

The Court Decides - And The Optionality Materializes

The legal uncertainty finally broke in the summer of 1963. On July 29, Chief Justice Sherwood Lett ruled that the government’s original seizure of British Columbia Electric had been unlawful and contrary to the constitution. He also concluded that the province had underpaid for the asset. Based on his assessment, compensation should have been set at C$192.8 million rather than the C$171.8 million already paid, using a multiple of roughly 17.5 times earnings and adding a modest premium to account for lost income.

Notably, the ruling stopped short of ordering the utility to be returned to British Columbia Power. That left the practical outcome unclear and forced both sides back to the negotiating table. Especially, if Bennett’s endeavours should not turn out to be pure illusionary.

British Columbia Power moved quickly. Management sent word to Premier Bennett that they were prepared to settle at a fair price. In the meantime, two procedural matters were scheduled before the court in early August: one request from the government to suspend proceedings while an appeal was considered, and another from British Columbia Power seeking to regain control of British Columbia Electric. Neither ended up being decisive. The hearings were postponed as negotiations between the province and the company gained momentum.

Rather than continue fighting, the two sides agreed to set boundaries for a settlement and to let Justice Lett determine the final amount within those limits. His decision came on September 27, 1963. He fixed total compensation for British Columbia Electric at C$197.1 million - roughly C$25 million more than what British Columbia Power had already received, or about C$5.30 per share. The difference between this figure and his earlier valuation was largely attributable to accrued interest.

Payment was made immediately, bringing the dispute to an end. As part of the settlement, the province also agreed to reimburse British Columbia Power for any debentures that might be presented for conversion, which effectively removed the last technical risk from the structure.

Liquidation: Turning Structure Into Cash

With the government payment in hand, British Columbia Power no longer had an operating business. It became a pool of cash with a winding-up plan - the purest form of a deep value liquidation investment. The company began distributing the proceeds to shareholders over several installments, with most of the money returned in the first liquidating distribution.

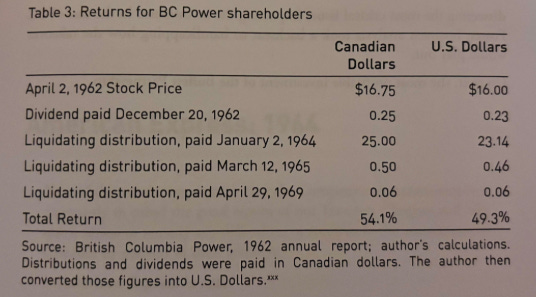

An investor who had bought shares around April 1962 at roughly C$16–17 received a sequence of cash flows that added up to a very respectable outcome: a modest dividend in late 1962, followed by a large liquidating distribution in early 1964, and smaller residual payments in the years that followed. In total, the investment generated a return of just over 50% in Canadian dollars, and just under that in U.S. dollar terms.

It was not a ten-bagger, but it was structured and low risk.

Why This Mattered for Buffett and Munger

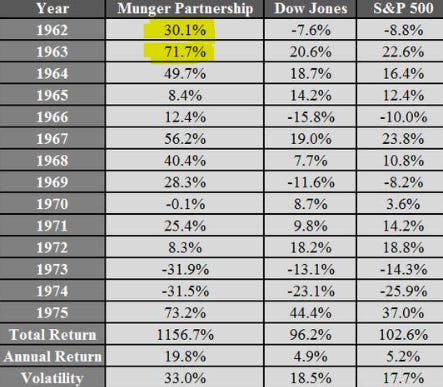

For Charlie Munger, this was an especially meaningful result. His partnership was newly formed, and British Columbia Power became one of its defining early successes. The position alone produced several hundred thousand dollars of profit and contributed materially to returns in both 1962 and 1963. He was off to a good start!

Munger was comfortable using leverage in this case, not because the situation was riskless, but because the downside was supported by arbitrage buyers who would step in if the price weakened. In effect, the market itself created a floor. He later remarked that he had not even known the term “risk arbitrage” at the time - he simply recognized that the odds were heavily skewed and so he made his fat pitch.

Buffett approached the situation with the same framework he used elsewhere. Whether the investment was a workout, a general stock, or a control situation, the process was identical: protect the downside, and demand an attractive payoff if things went right. British Columbia Power happened to fit that mold unusually well.

We do not know the exact day Buffett bought his shares, but we do know he owned them by the end of 1962, making it a very successful investment.

Closing the Loop

British Columbia Power ended the way workouts are supposed to end: not with a story, but with a cheque. It was not based on a operational turnaround, a decent management team or multiple expansion.

Just a sequence of legal steps, political compromises, and arithmetic.

It is easy to forget these kinds of investments because they leave no famous brand behind. But in terms of discipline and structure, this one is almost a textbook case of early Buffett deep value investing. It shows how mispricing can exist not because the future is unknown, but because the outcome is boring, technical, and hidden inside documents most people do not read.

And that is exactly why Buffett and Munger pursued this obscure workout and special situation investment.

Investments with no risk do exist, and I plan to publish one soon, which I believe fits the bill. One that found its way to my partner’s portfolio as well to close on the prologue.