A Special Situation Workout: Heads I Win, Tails I Don’t Lose Much

A Boardroom Coup By Activists Could Unlock 50–150% Upside The Early Buffett Way.

I promised to publish what I think fits the bill as a an asymmetric bet with large upside optionality after my British Columbia Power (Early Buffett-type workout) post - and here the opportunity is. Time to place your bets!

Today’s stock is one of my largest positions and within my pile of 5-7 companies comprising about 70-80% of my portfolio.

Summary

This is a deeply undervalued ASX-listed non-bank financial company with solid, cash-generative core operations. Trading at a distressed multiple due to corporate governance issues, it presents a rare special situation investment with asymmetric upside, attracting activist investors. The downside appears well protected by tangible assets, surplus cash, resilient earnings from secured lending and card portfolios, and an existing third-party indicative bid that anchors valuation near current levels. Even in a bear case where governance issues persist, the market is already pricing in extreme pessimism, leaving limited room for further multiple compression. The upside, however, is significant: a successful board reset and capital return program could unlock a rapid re-rating toward peer multiples, implying 50–100% upside without requiring heroic operating assumptions. Additional optionality exists through asset rationalisation, improved capital allocation, or a properly run M&A process that could surface higher bids. In effect, this sets up a rare “heads I win, tails I don’t lose much” situation, where governance - not earnings - determines the outcome.

I am Humm Group: an Australian Buy Now Pay Later (BNPL) company with a governance overhang but with decent prospects.

Overview

Humm Group is an Australian-based, undervalued non-bank financial services company, providing BNPL (Buy Now Pay Later) and SME lending solutions across multiple markets. The company operates across multiple markets including Australia, New Zealand, Ireland, Canada and the United Kingdom.

Under brands such as humm, humm90, Q Card and others, Humm offers buy-now-pay-later (BNPL) services, interest-free installment plans and credit card products that help individuals finance purchases ranging from everyday goods to higher-value items such as home renovation, healthcare and furniture. It also provides commercial financing solutions - including leasing and asset finance - for SMEs through its FlexiCommercial division.

Unlike a traditional bank, Humm doesn’t rely on customer deposits; it funds its lending activities through wholesale funding arrangements and securitisation partnerships while managing credit risk and servicing receivables via its technology and risk infrastructure.

BNPL Activities - Across Business and Geographical Segments

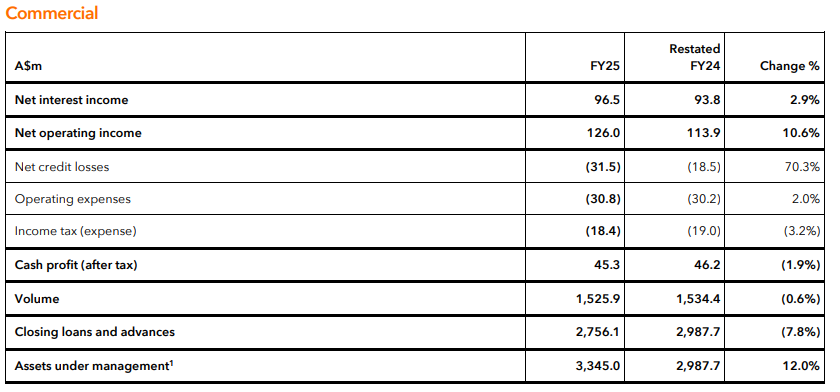

Commercial (Flexicommercial - Australia & New Zealand)

The commercial segment is Humm’s largest and most stable earnings engine with A$95.5m in net interest income (NII), focused on asset-backed lending to SMEs across Australia and New Zealand. The business operates primarily through broker and aggregator channels, offering equipment finance, vehicle finance and other secured lending products (chattel loans). A key strategic differentiator is its diversified funding model, including the recently established forward flow arrangement, which allows Humm to originate loans while recycling capital and reducing balance-sheet intensity, although only equalling about 11% of AUM.

In FY25, commercial delivered cash profit of $45.3m, broadly flat year-on-year despite a more challenging SME credit environment:

Credit losses increased as expected due to portfolio seasoning following strong growth in prior years. In other words, it is a lag-effect mainly because older loans are starting to show risk and because it’s taking longer to recover some secured loans, and certain sectors like Victorian transport. The credit losses incurred remain low in absolute terms and well within management’s expectations. Importantly, assets under management grew 12% to $3.3bn, demonstrating that the business continues to gain market share despite a contracting SME lending market. Overall, the commercial segment remains a high-quality, cash-generative pillar to Humm’s overall performance.

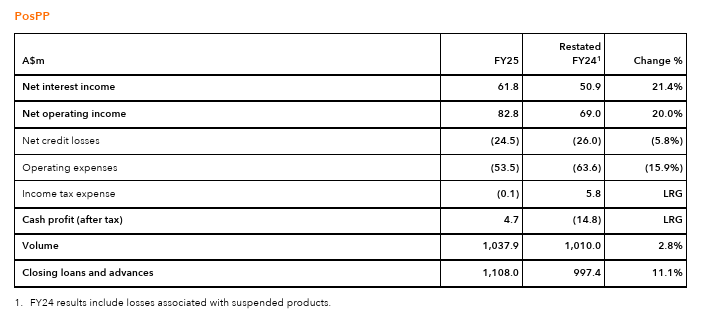

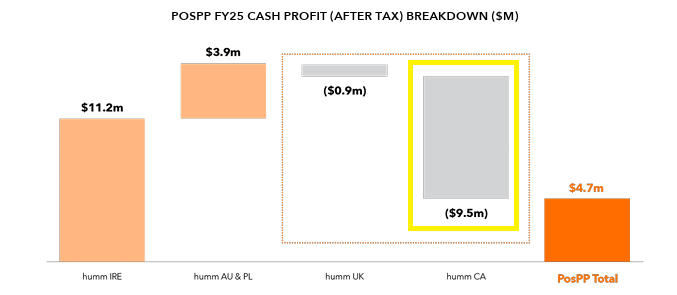

PosPP (Point-of-Sale Payment Plans - Australia, Canada, Ireland & UK)

The PosPP segment represents Humm’s growth-oriented consumer finance unit, offering point-of-sale installment products across multiple geographies. This includes the core Australian business alongside faster-growing international operations in Ireland, the UK and Canada. The segment has been undergoing material transformation in response to new BNPL regulations, with a strategic shift toward regulated, hybrid credit products (combination of traditional credit and BNPL-offerings) and vertical specialisation (focus on certain industries/segments). In turn, this also led the legacy “humm classic” product and platform to be placed into runoff and an impairment of $8.5m in software to be capitalised.

FY25 marked a clear inflection point for PosPP. The segment delivered cash profit of $4.7m, a significant turnaround-like reversal from a loss in FY24 (and there is more to come as a cliffhanger for later). This improvement was driven by strong growth in receivables, disciplined credit tightening, lower losses and a materially leaner cost base following the exit of suspended and legacy products.

Internationally, Ireland and the UK were the standout performers, delivering strongest growth at double-digit growth in loans and advances, coupled with improved unit economics and lower loss rates, albeit from a smaller base. The Canadian operations delivered lackluster performance.

In Australia, Humm accelerated the launch of its new regulated “humm” product, while placing the legacy “humm classic” platform into runoff as mentioned, which suppressed earnings.

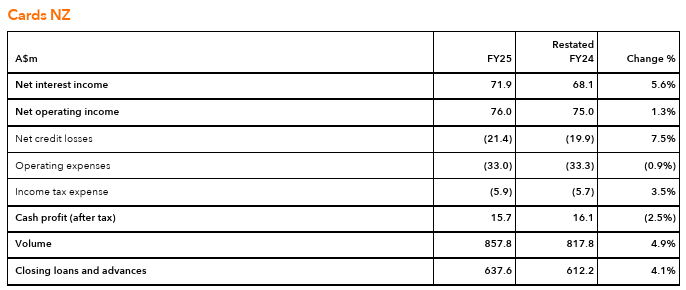

New Zealand Cards

The New Zealand Cards business is a mature, high-margin consumer lending franchise, anchored by well-established brands such as Q Card, Farmers Finance Card and co-branded Mastercards. It benefits from strong retailer relationships, pricing power and a loyal customer base, positioning it as a defensive earnings contributor within the group.

In FY25, the segment delivered cash profit of $15.7m, slightly below the prior year. This modest decline was largely due to higher funding costs rather than any deterioration in underlying business quality. Volumes grew nearly 5%, receivables increased, and interest income rose on the back of repricing initiatives.

Credit performance remained robust despite a challenging macro backdrop in New Zealand, with only a marginal uptick in loss ratios. Cost control was tight, and margins benefited from higher customer pricing. Overall, Cards NZ continues to function as a reliable, cash-generative asset, providing earnings stability and funding capacity for the broader group.

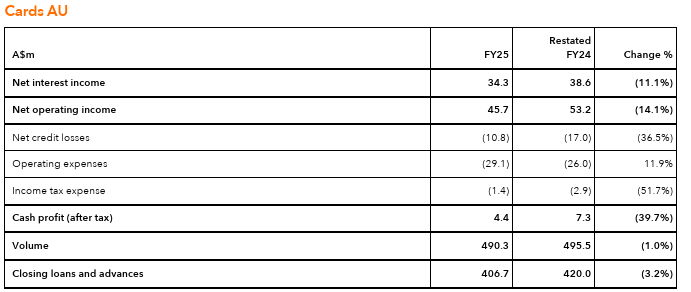

Australia Cards

The Australian Cards segment is a smaller, legacy portfolio that is currently being managed for optimisation rather than growth. The business operates on an ageing technology platform and is subject to heightened regulatory and legal scrutiny, which has shaped management’s conservative approach.

FY25 cash profit declined to $4.4m, reflecting elevated legal costs and a deliberate slowdown in customer acquisition. However, this strategic retrenchment has meaningfully improved credit quality, with net credit losses falling sharply year-on-year. Margins improved at the unit level, but this was insufficient to offset lower balances and higher fixed costs in the latest fiscal year.

The segment is effectively in maintenance mode ahead of a planned platform rebuild in FY26. While near-term earnings are subdued, management’s actions have reduced risk and preserved optionality, suggesting the downside is now largely contained for this segment.

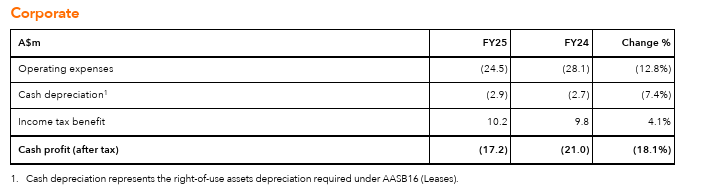

Corporate

The Corporate segment captures central group functions including finance, risk, technology, people and governance without a strong nexus to the business segments. While loss-making by design, it plays a critical role in enabling scale, regulatory compliance and platform transformation across the group.

In FY25, Corporate losses narrowed materially due to lower overheads and disciplined cost control, reflecting management’s broader focus on efficiency and simplification. The introduction of Corporate as a separate reporting segment improves transparency and highlights the underlying profitability of the operating businesses.

Funding and Capital

The company operates with a mature and well-diversified funding platform designed to support sustainable growth while maintaining a disciplined and capital-efficient balance sheet. As a non-bank financial institution, the group does not rely on customer deposits as mentioned earlier, but instead funds its lending activities through wholesale funding facilities, securitisation programs and capital markets transactions.

The funding strategy is centred on maintaining a committed, cost-effective mix of facilities while strengthening the group’s presence in debt capital markets. Humm accesses funding from a broad base of domestic and international banks and institutional investors, supported by long-established asset-backed securities (ABS) programs in both Australia and New Zealand.

During FY25, the company established a A$1.0bn Forward Flow program, under which A$682.8m of commercial loans were sold in two tranches. This structure is strategically important for the FlexiCommercial business, enabling capital recycling, reduced balance-sheet intensity and continued origination growth. In addition, an existing private placement facility was upsized by A$239.0m, while A$593.8m of notes were publicly issued under the Australian FlexiCommercial ABS program.

Within the consumer businesses, Humm issued A$196.1m of additional notes under an existing private placement to fund the Australian humm AU solar receivables portfolio. In New Zealand, NZ$369.0m of notes were publicly issued under the Cards master trust program. The group also completed the full repayment of its perpetual notes, with the remaining A$28.6m repaid in April 2025 following a partial repayment in December 2024.

At 30 June 2025, Humm had A$5.9bn of wholesale debt facilities funding its loan assets, with A$1.2bn of undrawn capacity. These facilities comprise a mix of public and private secured debt, backed by diversified pools of chattel loans, customer loans and finance lease receivables. A portion of the facilities operates on a revolving basis, allowing collections to be reinvested into new originations, while the remainder amortises in line with repayments of the underlying assets. The Forward Flow program provided a further A$0.4bn of undrawn capacity at period end.

Humm continues to actively optimize its capital structure, balancing liquidity, funding diversification and cost of capital. Opportunistic access to debt capital markets remains a key lever to expand funding capacity and lower overall funding costs. As at 30 June 2025, Humm had A$63.0m outstanding under its corporate debt facility, including A$3.0m of capitalised accrued interest.

A Discounted Valuation

As of today, Humm has 492,495,340 diluted shares outstanding and trades at a price of A$0.735/share, implying a market cap of A$361.98 million. Humm holds A$125.4 million in unrestricted cash on the balance sheet. Recent judgement related to the 2020-claim to SMBC was largely provisioned for and the recent Court judgment should only add A$3-4m in incremental costs. In other words this legacy risk is gone and should not oppress the large unrestricted cash pile. They have A$63.0m outstanding under its corporate debt facility, including A$3.0m of capitalised accrued interest. Real unrestricted net cash is around A$60m.

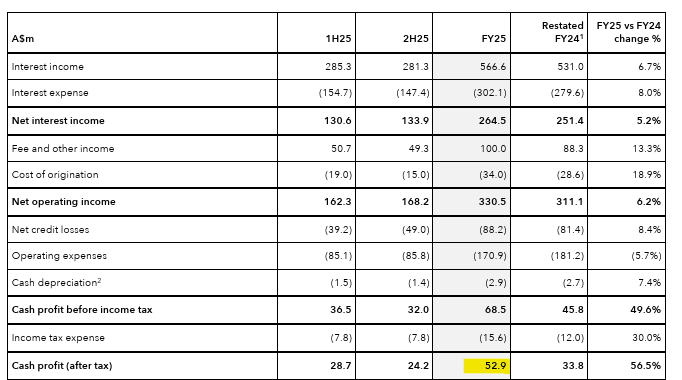

On aggregated basis, FY2025 delivered A$52.9 million on cash profit (after tax):

In relation to FY 2025, Humm seems to be trading at a P/E multiple of 6.84x and a P/E excluding unrestricted cash of 5.7x.

In relation to the PosPP-segment, we analyzed above it was clear that the Canadian operations were loss-making:

Also, it was worth noting that the “humm classic” product and platform were placed into runoff with an impairment of $8.5m. Coupled with easing of the portfolio seasonality like Victorian transport, I think cash profit on a more normalized basis and with some restructuring/reorganization efforts towards Canada will land in the area A$60-75 million. In turn, this would make Humm trade at a P/E of 4.8-6x or 4.0-5.0x times on P/E ex cash basis.

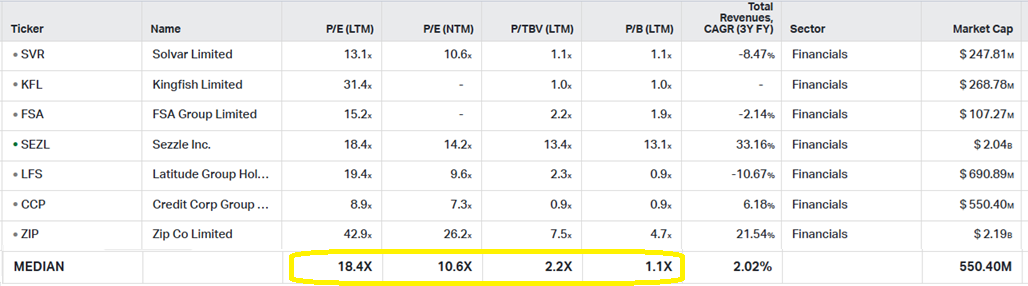

I consider this to be way too low compared with peers:

All peers does not necessarily constitute pure BNPL-comparables, but they gives us a hint as to how Humm should be valued. If we were to value Humm from this relative valuation, Humm should trade around A$636 to 973m based on LTM & NTM P/E ratios and from A$553 to 829m on price to book / tangible book (where goodwill and other intangible assets have been excluded). This would suggest a price of 1.08 to 1.91 Australian dollar per share - or an upside of 47 to 159%.

Humm has grown the topline the last 3 years at a CAGR of 14.4%, which is a bit less than Zip Co. and Sezzle Inc., but even if we omit these comps due to better growth prospects, we still find Humm to be trading lower than the peers on both P/E and P/B-basis.

The Reason to The Discounted Valuation

… terrible corporate governance with no respect given to minority investors.

I could leave it with that. But let us have a look into the past escapades of Humm.

Humm’s depressed valuation is best understood through the lens of corporate governance rather than operating performance. The roots of the problem trace back to August 2015, when Andrew Abercrombie became chairman. Since then, Humm’s share price has fallen by roughly 80%, even as the broader Australian equity market has risen by more than 50%. Over that decade, investor confidence has steadily eroded as governance concerns compounded.

Under Abercrombie’s chairmanship, the board has increasingly appeared misaligned with minority shareholders. The company cycled through six different CEOs, experienced repeated senior resignations, and ultimately lost five experienced non-executive directors following governance disputes. These issues came into sharper focus after the collapse of the proposed Latitude transaction in 2022, where five non-executive directors resigned. Abercrombie ran an aggressive campaign against the sale of this value-enhancing sale of the consumer division, it seemed.

More recently, governance concerns intensified following an opportunistic, low-ball MBO-takeover proposal from the chairman himself in mid-2025 at a crazy low price of A$0.58 a share. Rather than immediately rejecting the offer and testing the market, the board’s so-called ‘‘independent board committee’’ engaged in prolonged due diligence for more than three months. The committee should have immediately rejected the proposal from the chairman, calibrated with the market for competing offers, but the committee was not independent at all. It comprised three ‘‘independent’’ directors and ALL appointed by Mr. Abercrombie himself.

Further damage was done by opaque decision-making around financial disclosures, dividend policy, and capital allocation, including disputes over the FY25 accounts and the handling of a subsequent, higher indicative proposal from Credit Corp, although 33% higher than Abercrombie’s low-ball offer (bid reflecting a price of A$0.77 a share). At each step, the board’s actions appeared defensive, slow, and reactive - deepening the governance overhang.

As a result, the market has come to apply a structural discount to Humm’s shares. Despite decent growth in topline and earnings, surplus capital, and a balance sheet capable of supporting materially higher dividends and buybacks, investors remain sceptical that value will ever be returned while the current board remains in place. In effect, governance risk - not earnings power - has become the dominant driver of valuation.

This is hopefully about to change.

Shrewd Activists Pounce Back

By December, activist investor Jeremy Raper had enough. After almost six months of sparring with the board (for instance he wrote a letter to the IB committee in June 2025), he moved to trigger a long-foreshadowed board spill at Humm.

Together with Collins St Asset Management, Jeremy is calling out fellow shareholders with a letter by the title: ‘‘END THE CIRCUS - OVERHAUL THE HUMM BOARD’’ in late December ‘25.

In summary, they criticize Abercrombie’s low-ball offer, lack of independence on AGM’s, refusal to approve FY25 accounts when Abercrombie was trying to takeover the company and the handling of the Credit Corp offer. Generally, they argue these events demonstrate a largely captive board with no true independence from the chair; and a corporate governance culture that is fundamentally broken and not fit for purpose.

Regarding the low-ball offer, they estimate Abercrombie’s failed bid valued Humm at 4.4x last LTM EPS and at around 0.75x price to net tangible assets, meanwhile no listed non-bank financial services company trades below 10x LTM EPS or below 1-2x P/NTA in the peer group.

They propose:

a fully-franked special dividend of at least A$15 million;

a 10% share buy-back over the next 12 months;

a clarified dividend policy that establishes a payout ratio of at least 75% of underlying earnings, reflecting a mid-teens dividend yield;

a restructuring or exit from the loss-making Canadian operations;

ongoing board renewal via the appointment of a further 1-2 independent directors;

a full and complete review of the actions and decisions of the previous board over the past 12 months; and

engage former LT non-executive director Rajeev Dhawan as a strategic board consultant. His deep experience with Humm will be invaluable assistance to their turnaround plan (e.g. the Canadian operations).

Another letter followed to the Audit and Risk Committee’s chair Mr. Robert Hines. This letter alleges serious corporate governance failures relating to the approval of the Humm chairman’s large on-market share purchases in December 2025.

It argues that the trades should never have been permitted given the high risk of actual or perceived insider trading, as they occurred during an active takeover process, near the end of a trading quarter, and amid an imminent board challenge.

Jeremy questions whether the company’s securities trading policy was properly followed, including whether the required prior notice was given and whether the Audit and Risk Committee chair formally approved the trades. Finally, the letter demands on-the-record answers and warns that, if the current board renewal succeeds, a full retrospective governance review will be conducted and disclosed to the market.

The Catalyst: The Upcoming EGM

The activists and corporate governance protagonists organizes a general meeting to be held the 19th of February with 6 resolutions on the agenda:

Appointment of Mr. Jeremy Michael Kersten Raper

Appointment of Mr. Garry Roy Sladden

Removal of Mr. Andrew Abercrombie as a Director

Removal of Mr. Robert Hines as a Director

Removal of Mr. Andrew Darbyshire as a Director

Removal of any other persons as a Director

This makes the case a perfect activists and special situations’ investment as Garry and Jeremy seems to be the solution to the governance overhang:

Garry Sladden

Garry Sladden is an experienced non-executive director and chairman with more than 20 years’ board experience across private and ASX-listed companies. A former senior executive at Consolidated Press Holdings, he has extensive experience navigating complex governance situations, founder-led businesses, and corporate turnarounds. He is currently Non-Executive Chairman of Ignite Ltd (ASX: IGN) and has led multiple successful restructurings and growth strategies across diverse sectors.

Jeremy Raper

Jeremy Raper is the third-largest shareholder in Humm, holding 5.8% of the company, with interests closely aligned with other shareholders. He manages Raper Capital, a single-family office, and has over 20 years’ experience across buy- and sell-side investing, including a strong track record of constructive shareholder engagement in small-cap companies. He holds a cum laude degree in History from Harvard University.

As promised in the letter to shareholders, they will work towards an immediate return of capital through a fully franked special dividend of at least A$15 million and a 10% on-market share buy-back, alongside a clearer dividend policy targeting a payout of at least 75% of underlying earnings. Further, to seek decisive action on underperforming assets, including a restructuring or exit from the loss-making Canadian business. In addition, they will conduct a comprehensive review of the prior board’s decisions over the past year, and engage the former non-executive director Rajeev Dhawan as a strategic board adviser to support the turnaround. I assume this refers to the Canadian loss-making division among others. Restructured, it will boost earnings / cash profit to the A$60 to 75m area as also mentioned in the valuation part.

The upcoming EGM represents a clear inflection point: either the governance discount persists, or the conditions are finally created for a rerating.

The Asymmetric Bet

Let us be honest: Humm is under-valued and dirt cheap for a reason. It is in need of a corporate governance overhaul and I think Jeremy Raper along with fellow activists and shareholders may achieve this.

If they succeed, Humm should set up for a decent re-rating to a price of 1.08 to 1.91 Australian dollar per share - or an upside of 47 to 159%. This is our upside optionality not even considering further execution and operational performance.

The re-rating should originate from the following avenues:

Ordinary re-rating from market appreciation

Shareholder yields: buybacks and dividends from the large unrestricted net cash level

Other avenues to maximize shareholder value in the near- and medium-term, like engaging with Credit Corp (and any other third-party) in good faith i.e. a clear and ordinary M&A process where materially higher hostile bids may emerge

The downside will reflect the situation where EGM resolutions are not to be materialized, although I think there will be a good chance. For instance, past voting suggests that shareholders have not been satisfied - a good recent example was the latest remuneration report, where more than 50% of the votes were against.

Further, Jeremy and the other activists have taken necessary steps to call out all shareholders through ‘‘Humm Board CleanOut’’ and other gateways.

Still, in the scenario where the resolutions are not met, I still think the downside should be protected from:

The already low multiple paid

The offer from Credit Corp at A$0.77 a share, although non-binding

Lessons learned for the existing Humm board, including Mr. Abercrombie, increasing the likelihood of a higher management buyout bid or more constructive engagement with Credit Corp and third-party acquirers.

Do Not Forget to Vote

At current levels, Humm presents a highly asymmetric opportunity. If the activists succeed at the upcoming EGM, the removal of the governance overhang alone should unlock a meaningful re-rating, with additional upside from capital returns and strategic optionality, including a properly run M&A process.

If they fail, the downside appears limited by an already depressed valuation, tangible asset backing, and an existing third-party indicative offer.

In short, this increasingly resembles a rare “heads I win, tails I don’t lose much” situation - but the upside optionality only materialises if shareholders make their voices heard.

Do not forget to vote at the EGM as Humm trades at a distressed multiple compared to peers. With activist-driven governance reforms, the company shows significant upside potential and a rare risk-reward asymmetric investment opportunity.

I hold shares in the security mentioned and may transact in the shares at any time, including prior to or following the publication of this article. Always do your own due diligence. This writeup does not constitute personalized investment advice, a recommendation, or a solicitation to buy or sell any security.

The Bargain Ticker is a publication and only for informational and educational purposes.

This is a great write-up. You do a really clear job separating operating strength from the governance discount, and the way you frame the EGM as the true catalyst makes the asymmetry obvious. Feels very true to the “early Buffett workout” lens you referenced.

I came across this company 7-8 months ago and ruled it out mainly due to governance issues (which, in hindsight, may have been the "wrong" call given the stock’s performance since).

Glad to see things are moving in a tangible way. I’ll take a deeper look, this looks genuinely interesting, and I’m going to dig into it. I also appreciate how much Jeremy Raper is personally invested in this.

Great deep dive, thanks for sharing it with us!